Capital in the 21st Century

by Thomas Piketty

Translated by Arthur Goldhammer

The Belknap Press of Harvard University Press, 2014

ISBN 978-0674430006

$39.95/£29.95

Capital in the 21st Century

by Thomas Piketty

Translated by Arthur Goldhammer

The Belknap Press of Harvard University Press, 2014

ISBN 978-0674430006

$39.95/£29.95

I'm reviewing this book on wealth and macroeconomics in the spirit of French economist Thomas Piketty's own desire to see his thesis on 'political economy' become part of public debate (p574), in the full knowledge that I personally bring little in the way of expertise to the table. I think it's fair to say, though, that this 685 page whopper is itself equivalent to taking a short university course in economics. Piketty is, after all, a professor (directeur d'études) at the École des hautes études en sciences sociales (EHESS) and at the Paris School of Economics, so you'd expect nothing less.

This book made a big impact in 2014 at a time of austerity across much of Europe, in the wake of the financial crash of 2007-8 as well as the ongoing problems in the Eurozone. The book puts the current economic trends (particularly regarding wealth) into a more long-term perspective, drawing much-needed lessons from history. This was not as easy as one might expect, as historical economic data is often fragmentary, even non-existent in many countries - at odds with what one might expect given the modern churn of data we've all become accustomed to. So, the first section of the book provides much-needed historical data from the last three centuries, meticulously sourced by Piketty's diligent research team.

The best data available is from France and Britain, whose historical records provide the best level of consistency and detail over that length of time. These two countries provide the basic template to see how trends changed in the 19th and 20th centuries, but Piketty also examines many other countries too, including the United States.

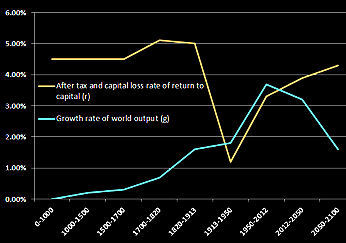

Table 1: Historical comparison of rate of return on capital versus growth and projected through the 21st Century

A consistent picture emerges which questions some of the basic assumptions we tend to make about the role of wealth in modern times. Essentially, the emerging patterns of the last 35 years suggest a return to an economy more in keeping with that of the 18th and 19th century than the more egalitarian period of 'les trente glorieuses', post-WWII period. Wealth is once again becoming the predominant economic factor in Western economies with a steady rise in wealth inequality reshaping economic distribution. This is nothing particularly new in Europe, just a return to 'the old days'; but this transition represents something more novel in the United States, whose meritocratic principles are increasingly being challenged by the relentless coring out of their middle classes.

Piketty's scientific observation that Wealth Is Back has made sense of a change in the British economy that has been personally puzzling me for some years. Back in my young adulthood, when you came to buy a house (perfectly normal back then...) the important deciding factor on what you could afford was the ratio between house price and earnings, which was then consistently about 2.5 to 3. Now, it is somewhere between 5 and 10, depending upon what part of the country you live in. So, why, I've often asked myself, has the British housing market not crashed, or at least undergone a reasonable adjustment?

The answer is the fundamental upward shift in the ratio between return from capital and growth. The top decile (and, more so, centile) of wealth distribution is holding an ever-increasing slice of the pie, and they're using their wealth to buy up ever more of the available capital from a relatively stagnant economic base. The result is that more of the finite real estate is being bought up by what Piketty calls wealthy 'rentiers' (we British might use the term landlords) the impact of which is distorting the housing market to such an extent that income (and the relatively meagre savings from it) is no longer sufficient to afford a house. Hence, in popular property TV shows like 'Location, Location, Location', we see chic, well-heeled Londoners discovering to their horror that their half-a-million quid barely buys a modest flat in a so-called 'up-and-coming' borough. As for 'normal' working Londoners, well, forget it...

That's not to say that there won't eventually be a crash, but what would otherwise appear to be an unsustainable housing bubble is more likely perfectly sustainable through the mass acquisition of property by very, very wealthy capitalists. In other words, we're rapidly heading right back to Victorian times, opening the door for a future filled with Dickensian horror.

"Modern meritocratic society, especially in the United States, is much harder on the losers, because it seeks to justify domination on the grounds of justice, virtue, and merit, to say nothing of the insufficient productivity of those at the bottom." (p416)

Piketty prefers to quote Balzac and Austen in his study of 18th and 19th century low growth, low inflation 'Belle Epoque' European economies; but Dickens may be where it's at, I fear. The 21st Century will see (is seeing...) a return to low growth in the West, where capital and inherited wealth will increasingly dominate the economy, which will have a huge impact on the lives of the younger generation today:

"...Younger people, in particular those born in the 1970s and 1980s, have already experienced (to a certain extent) the important role that inheritance will once again play in their lives and the lives of their relatives and friends. For this group, for example, whether or not a child receives gifts from parents can have a major impact in deciding who will own property and who will not, at what age, and how extensive that property will be... Inheritance is playing a larger part in their lives, careers, and individual and family choices than it did for the baby boomers." (p381)

Piketty shows that this propensity for increased 'gift-giving' is not as prevalent in the UK as elsewhere, and wonders why. I'm not as surprised, to be honest: So much of Britain's private wealth is tied up in its housing stock that more liquid assets available for familial redistribution to the next generation are in short supply. Furthermore, the older generation seem almost wilfully ignorant of the sea-change in home-ownership patterns going on around them...largely because they themselves are completely unaffected by it. Indeed, many have taken full advantage to become 'petit rentiers' themselves, to the detriment of the next generation.

Again, this return to the economic reality of 'Old Europe' has a cultural familiarity to it that most Europeans will relate to, but it is the emergence of this reality in America, which has prided itself upon its meritocratic dynamism, that is going to hurt the most. The rise of the 'supermanager' in the Anglo-Saxon economies has provided Wealth with a certain amount of cover. CEOs of top Anglo-Saxon companies make annual fortunes that their predecessors only a decade or two ago could only have dreamt of. Does this not reflect a true meritocracy, where fortunes are accumulated rightly by the top talent? To some extent, Piketty concedes, this is justifiable, but he points out also that the performance of the Anglo-Saxon companies is no better than continental Europe's, or Japan's, which offer no such distortions in their remunerative distributions. Besides, he argues, it's the eventual inheritance of that immense top-centile wealth by their children that will drive America and Britain ever further into a patrimonial, rentier-dominated economy; a shift not without consequences:

"The world to come may well combine the worst of two past worlds: both very large inequality of inherited wealth and very high wage inequalities justified in terms of merit and productivity (claims with very little factual basis, as noted). Meritocratic extremism can thus lead to a race between supermanagers and rentiers, to the detriment of those who are neither." (p417)

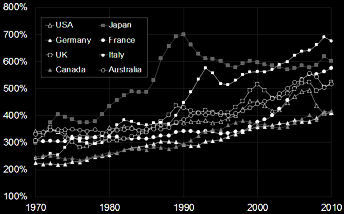

Table 2: Private wealth/national income ratios, 1970-2010.

voxeu.org/article/capital-back

One of the other issues which Piketty addresses in the book is public debt, a problem rife across Western economies. The usual way of dealing with this kind of debt is through inflation. However, right now the West, if anything, is heading into a deflationary spiral, which exacerbates the difficulty governments face when trying to rid themselves of their ballooning deficits. The lack of political and fiscal cohesion in Eurozone countries makes this all the more difficult for the already creaking single currency.

Piketty shows that public deficits have risen at exactly the same time as private capital to GDP ratios have grown. In other words, private wealth is growing alongside public debt. It's curious, he muses, how indebted Western societies prefer to borrow from their wealthy citizens (paying them back with interest on safe government bonds) than simply tax them outright for the same money. Instead, there is a fiscal rush to the bottom among competitor countries, each vying with the other to attract wealthy individuals to park their money in their low-tax-base economy.

Actually, though, a goodly fraction of that money is simply disappearing year-by-year from the global balance sheet. Piketty wryly notes how chronic Western balance-of-payments deficits are not matched by surpluses in developing nations. The money goes elsewhere. It's as if Earth is owned by Mars, he jokes. Of course, the real black holes lie in the Tax Havens. Tax Havens aren't the countries defending us from an ever emboldened Russia, or the Islamofascism spreading across the Middle East. Personally, I'd argue they should defend themselves rather than hiding behind a NATO defensive shield they themselves have decided not to contribute towards. As much as I wouldn't like to see Putin 'defending the interests' of ex-patriot Russki oligarchs in Monaco, I'd have little sympathy for the Principality's whining if he did park his Black Sea fleet in their over-gilded port. Pay your bloody taxes.

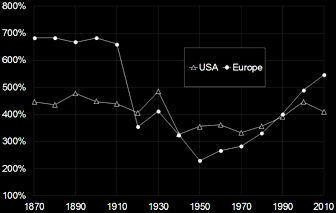

Table 3: Private wealth/national income ratios, 1870-2010: Europe vs. USA

voxeu.org/article/capital-back

So what is the answer to this downward spiral? Piketty argues that the patrimonial society of Old Europe is in reality the norm. The mid-section of the 20th Century was an abnormal period of egalitarian high-growth economic progress which fundamentally redistributed capital because the World Wars and the Depression essentially destroyed a large chunk of the West's capital base, either through direct means or, more so, high levels of taxes on the wealthy to pay for them. High growth and inflation then lead to greater meritocracy, where income from labour trumped income from capital. Demographic growth, particularly in the US, fuelled this economic model still further. Those times are now past. Controversially, Piketty argues that the market will not self-correct back to this kind of economy: The 'trente glorieuses' were the aberration, not the norm.

If the book wasn't already controversial enough, we move towards the French economist's recommendations. Having explored various fiscal solutions which would likely fall short of preventing a return to a patrimonial society, Piketty advocates a global progressive tax on capital. This could be done either as a one-off tax, or as a much lower rate annual tax. The simple message is to tax the wealth of the very rich to clear up the burgeoning public deficit. This kind of tax would require close global cooperation between all governments. Well, as much as I'm sympathetic to his description of the problems we face economically going forward, this solution is cloud-cuckoo land. It simply isn't going to happen.

Where there is practical scope for change, I think, is through progressive taxes on income, and on inheritance (p513). Fiscal regimes needs to reflect the changing wealth inequalities emerging in our societies. The top centile need to have their wealth capped to prevent major problems down the road, that much is clear, but a tax on capital itself is not the way to go. A progressive inheritance tax (which ran at very high levels in both the UK and US in the middle of the 20th Century) maintains a meritocratic dimension, because those whose talents have earned them wealth are not unduly burdened by the tax themselves. But caution is needed.

As noted above, we already have a changing landscape of capital where inheritance is playing an increasingly important part in helping the younger generation to get on the first rung of the housing ladder. Clearly, such a tax needs to be progressive, not regressive. Properly managed, it should prove effective, especially with regards to property. After all, houses cannot be moved to tax havens, and so property taxes are not subject to the kind of mass syphoning-off of resources that rich folk can easily manage with their liquid assets. However, as a millionaire's wealth increases (x10m, x100m), the capital they own tends to be made up less with just their own home - as extravagant as that may be - and increasingly is taken up portfolios of stocks and shares. Again, I would say his argument for a capital tax on those business interests are neither warranted nor desirable - they would simply drive a coach and horses through the entire stock exchange system, with extremely dangerous consequences for us all.

This is a truly remarkable book, and I learned so much from it. There are lessons here that can shape our own futures as we learn to recognise how the economic reality of our societies is changing, and how we have to adapt to it. I say that, because I don't think that the fiscal solutions Professor Piketty offers are sufficiently pragmatic to be remotely achievable, and his fairly gloomy predictions about where we're heading seem likely to become a reality. It seems that the lesson from history is that only a European war of epic proportions can shift us back to an egalitarian economy - a solution which is also far from welcome. Capital is back!

![]() You can order your copy through Amazon.com here:

You can order your copy through Amazon.com here:

Capital in the Twenty-First Century

![]() If you live in the UK, you can obtain your copy through Amazon.co.uk here:

If you live in the UK, you can obtain your copy through Amazon.co.uk here:

Capital in the Twenty-First Century

Book review by Andy Lloyd, 15th February 2015

Books for review can be sent to Andy Lloyd at the author/publisher's own risk.

Book Review Listings by Author and Title

Book Review Listings by Subject